I’ve recently posted several strategy scripts to the website that identify quantifiable edges for my fellow traders. These ThinkOrSwim trading strategies can be traded standalone, or tweaked further and customized to fit an individual’s trading style. They can either be used to setup automated trading systems in other platforms, or traded manually within ThinkOrSwim and improved with price action trading principles. My most recent strategies are all listed under the strategies category on the site, and here’s a quick reference list:

Most of these strategies come straight out of Larry Connors and Cesar Alvarez’s book “Short Term Trading Strategies that Work,” and are specifically for trading the SPY, SPX, or ES futures. But these ThinkOrSwim trading strategies may also provide edges on other instruments, and you can test them on whatever symbols you like to trade, to see if they can be applied profitably there as well.

I hope these strategies are as intriguing to you as they were to me, and hopefully they will provide you a more quantifiable way to determine your edge in the market as well.

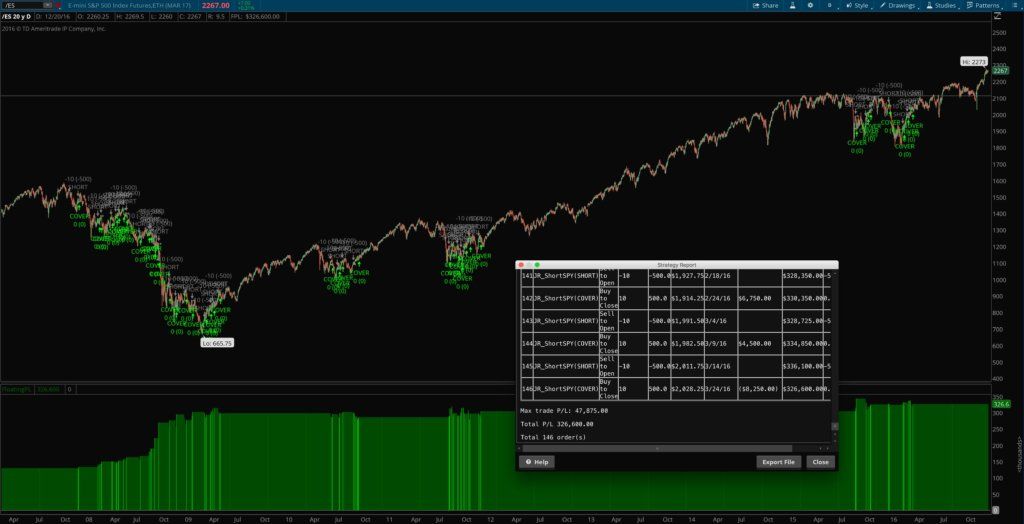

The short SPY trading strategy comes straight out of Larry Connors’ & Cesar Alvarez’s book called “Short Term Trading Strategies that Work” and it’s the one strategy that they present for shorting. I’ve really been enjoying programming and testing some of the ideas presented in their book — a lot of which seem to have some merit — so I wanted to go ahead and share some of the work I’ve been doing with my readers.

The default settings that the trading strategy comes with are straight out of the book on page 106, and seem to perform very well in my own tests, but they can be easily customized and tested with different values using the strategy properties menu. This is useful for quickly backtesting the strategy with different instruments, time frames, and market conditions.

The original strategy in the book calls for no stop to be used, but I went ahead and added the option for a percentage based stop to make the strategy more applicable to different trading styles and time frames.

Results from thinkorswim strategy backtests can easily be exported and analyzed further in Excel or other spreadsheet programs simply by right-clicking on a strategy signal on the chart and clicking “Export” in the popup menu.

The Authors’ Stats:

Instrument: SPY

Win Rate: 68.75%

# Trades: 16

Points gained: 169.91

Avg. Holding Time: under 5 days

What You Get

Short S&P strategy file for thinkorswim from page 106 of the book

All parameters are customizable in the properties menu

Option to use a stop or not to use a stop, and to set the size in %

Customizable colors

Why You Want It

The high win/loss ratio on the SPY and other instruments makes it an easy strategy to trade from a psychological standpoint

Includes the option to add a stop, which makes the strategy even more easy to trade

Ability to quantitatively backtest the strategy on multiple instruments, timeframes, and conditions affords more peace of mind and encourages traders to fully trust in their system.

How it Works

The strategy is straightforward: just make sure the market is under the 200 day sma, and then if the market makes 4 new higher closes, sell the market and cover once it drops below its 5 day sma. Traders can optionally add a percentage based stop to the strategy (simple option in the properties menu) and customize how big the percentage stop should be.

$69.99Original price was: $69.99.$49.99Current price is: $49.99.Add to cart

Cumulative RSI (3) Trading Strategy for ThinkOrSwim

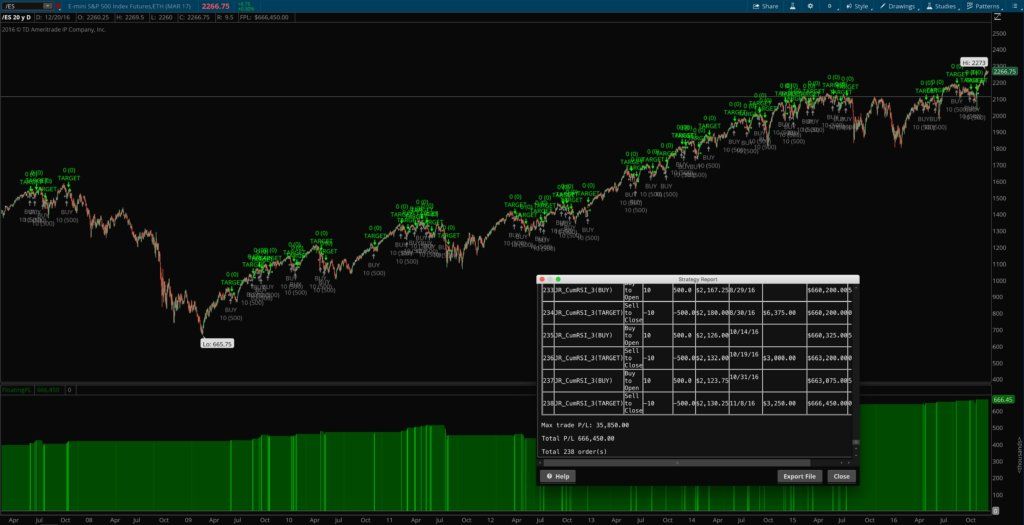

The cumulative RSI strategy comes straight out of Larry Connors’ & Cesar Alvarez’s book called “Short Term Trading Strategies that Work“. I’ve really been enjoying programming and testing some of the ideas presented in their book — a lot of which seem to have some merit — so I wanted to go ahead and share some of the work I’ve been doing with my readers. On page 104 of their book, Connors and Alvarez state that this strategy was 79.49% accurate on the SPY when tested, earning 779.51 S&P points with an average holding period of under 5 trading days.

There are 2 cumulative RSI strategies in the book. This particular strategy is Connors’ example of a different way of using his favorite tool, the cumulative RSIs, with a slight longer look-back timeframe. For the first version, which is also a strong contender, check out the other cumulative RSI strategy page here.

The default settings that the trading strategy comes with are straight out of the book on page 104, and seem to perform very well in my own tests, but they can be easily customized and tested with different values using the strategy properties menu. This is useful for quickly backtesting the strategy with different instruments, time frames, and market conditions.

The original strategy in the book calls for no stop to be used. But I added the option for a percentage based stop to make the strategy more applicable to different trading styles.

Results from thinkorswim strategy backtests can easily be exported and analyzed further in Excel or other spreadsheet programs simply by right-clicking on a strategy signal on the chart and clicking “Export” in the popup menu.

The Authors’ Stats:

Instrument: SPY

Win Rate: 79.49%

# Trades: 78

Points gained: 779.51

Avg. Holding Time: under 5 days

What You Get

Cumulative RSI(3) strategy file for thinkorswim from pg. 104

All parameters are customizable in the properties menu

Option to use a stop or not to use a stop, and to set the size in %

Customizable colors

Why You Want It

The extremely high win/loss ratio on the SPY makes it an easy strategy to trade from a psychological standpoint

Option to add a stop makes the strategy even more easy to trade

Long-only strategy further makes it even easier to trade for almost anyone, regardless of what type of account they trade out of

Ability to quantitatively backtest the strategy on multiple instruments, timeframes, and conditions affords more peace of mind and encourages traders to fully trust in their system.

How it Works

The cumulative RSIs strategy first makes sure the instrument is in a long term uptrend (with customizable parameters), and then takes the sum of the past x-number of RSI(y) values and if the number is sufficiently oversold, the strategy issues a buy signal, and if it then subsequently becomes sufficiently overbought, it issues a sell to close signal. The overbought and oversold levels can be customized as needed. Traders can optionally add a percentage based stop to the strategy (simple option in the properties menu) and customize how big the percentage stop should be.

$69.99Original price was: $69.99.$49.99Current price is: $49.99.Add to cart

$69.99Original price was: $69.99.$49.99Current price is: $49.99.Add to cart

Josiah is a stock & futures trader, ThinkScript programmer, Bitcoin maximalist, gold bug, real estate investor, and budding mountaineer. He's also rumored to be an in-shower opera singer. Josiah started Easycators in 2014 and lives with his family near Nashville, TN. xTwitter | YouTube

This website uses cookies to improve your experience. We'll assume you're okay with this, but you can opt-out if you wish. Accept | Read More

Privacy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.