The Short SPY Trading Strategy for ThinkOrSwim

The short SPY trading strategy comes straight out of Larry Connors’ & Cesar Alvarez’s book called “Short Term Trading Strategies that Work” and it’s the one strategy that they present for shorting. I’ve really been enjoying programming and testing some of the ideas presented in their book — a lot of which seem to have some merit — so I wanted to go ahead and share some of the work I’ve been doing with my readers.

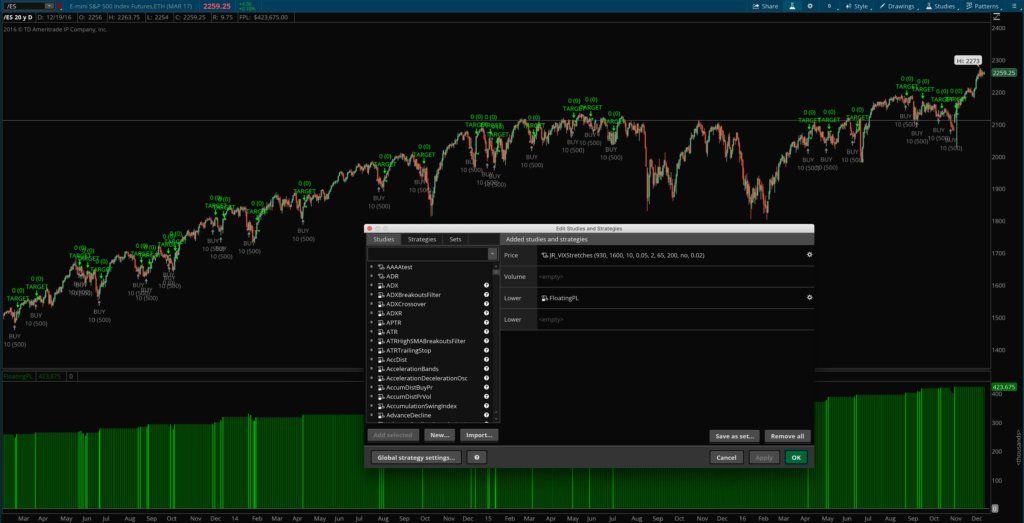

The default settings that the trading strategy comes with are straight out of the book on page 106, and seem to perform very well in my own tests, but they can be easily customized and tested with different values using the strategy properties menu. This is useful for quickly backtesting the strategy with different instruments, time frames, and market conditions.

The original strategy in the book calls for no stop to be used, but I went ahead and added the option for a percentage based stop to make the strategy more applicable to different trading styles and time frames.

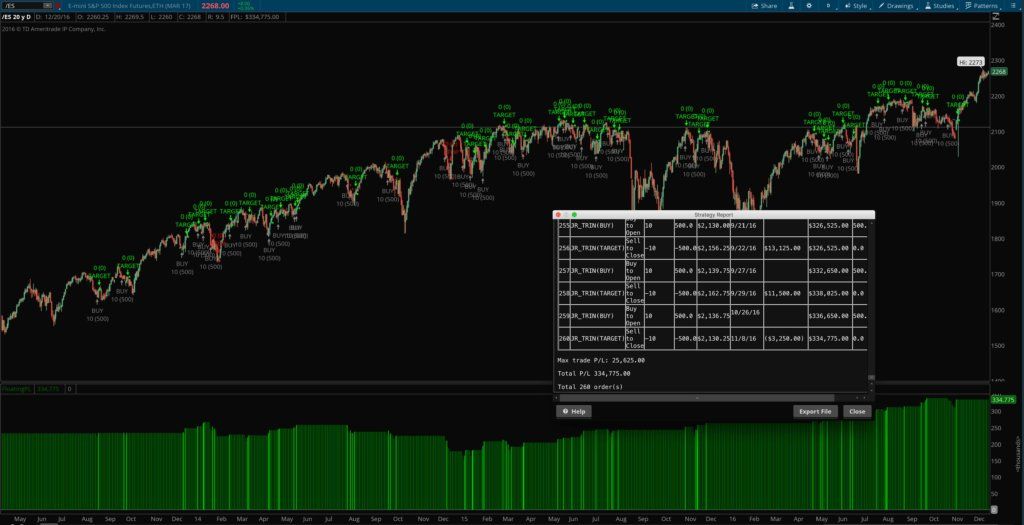

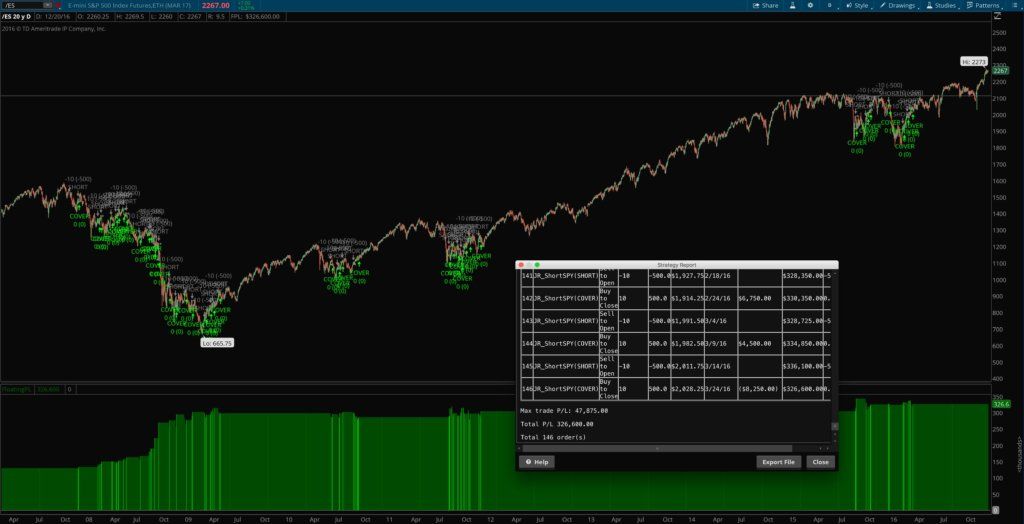

Results from thinkorswim strategy backtests can easily be exported and analyzed further in Excel or other spreadsheet programs simply by right-clicking on a strategy signal on the chart and clicking “Export” in the popup menu.

The Authors’ Stats:

- Instrument: SPY

- Win Rate: 68.75%

- # Trades: 16

- Points gained: 169.91

- Avg. Holding Time: under 5 days

What You Get

- Short S&P strategy file for thinkorswim from page 106 of the book

- All parameters are customizable in the properties menu

- Option to use a stop or not to use a stop, and to set the size in %

- Customizable colors

Why You Want It

- The high win/loss ratio on the SPY and other instruments makes it an easy strategy to trade from a psychological standpoint

- Includes the option to add a stop, which makes the strategy even more easy to trade

- Ability to quantitatively backtest the strategy on multiple instruments, timeframes, and conditions affords more peace of mind and encourages traders to fully trust in their system.

How it Works

The strategy is straightforward: just make sure the market is under the 200 day sma, and then if the market makes 4 new higher closes, sell the market and cover once it drops below its 5 day sma. Traders can optionally add a percentage based stop to the strategy (simple option in the properties menu) and customize how big the percentage stop should be.

Original price was: $69.99.$49.99Current price is: $49.99.Add to cart